|

||||||||||||

LENOX GROUP INC REPORTS FIRST QUARTER 2007 RESULTS -

(VIEW OR DOWNLOAD PDF)

May 7, 2007 – Eden Prairie, MN – Lenox Group Inc (NYSE: LNX), a leading tabletop, giftware and collectible company, today reported financial results for its first quarter ending March 31, 2007.

Summary of Results

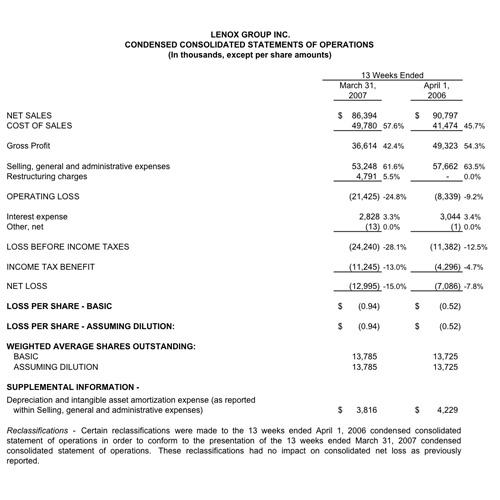

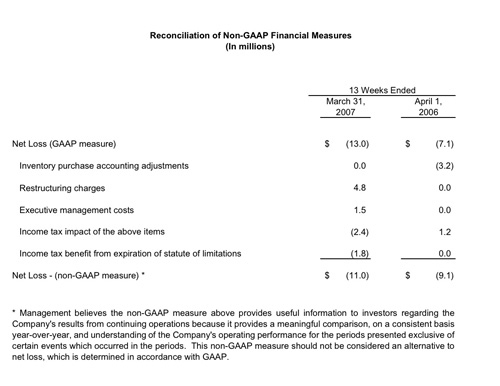

Revenues for the first quarter were $86.4 million compared to $90.8 million in the first quarter of 2006, largely reflecting a $3.2 million decline in the Company’s Direct segment and a $1.5 million decline in its Wholesale segment. The net loss for the first quarter was $13.0 million, or $0.94 per share, compared with a net loss of $7.1 million, or $0.52 per share, in the first quarter of 2006.

The comparability of the net loss for the first quarter of 2007 to the same period in 2006 was impacted by certain restructuring and other costs incurred in 2007, a tax benefit recognized in 2007 and a purchase accounting benefit recognized during 2006. Contributing to the increase in the net loss during the first quarter of 2007 were restructuring costs of $4.8 million and executive management costs of $1.5 million, partially offset by a separate $1.8 million after tax benefit as a result of the expiration of the statute of limitations on certain tax positions the Company had previously taken. The first quarter of 2006 benefited from certain purchase accounting adjustments to inventory of $3.2 million. Excluding the aforementioned items and their related tax effect, the net loss for the first quarter of 2007 was $11.0 million or $0.80 per

share compared to a net loss of $9.1 million or $0.66 per share during the first quarter of 2006. This presentation of the net loss and net loss per share are non-GAAP measures. Management believes these non-GAAP measures provide useful information to investors regarding the Company’s results because it provides a more meaningful comparison and understanding of the Company’s operating performance compared to last year. These non GAAP measures should not be considered an alternative to the results from operations which are determined in accordance with GAAP. A reconciliation of the GAAP financial measures to the non-GAAP financial measures is attached.

Marc Pfefferle, interim Chief Executive Officer said “As we discussed in our call with investors two weeks ago, since the beginning of the year, we have developed a new business plan and have made substantial progress in implementing business improvements based on that plan, including financial, operational and organizational changes. We are creating a brand-focused organizational structure and positioning the Lenox Group portfolio of brands for success by, among other things, reducing operating costs, eliminating organizational inefficiencies and streamlining processes. Overall, our first quarter results were slightly better than our plan, however, we clearly need to improve on them. Our business improvement initiatives will have a greater impact as the year progresses. In 2007, we will be focusing on setting the stage for the Company’s future growth and profitability.

Refinancing

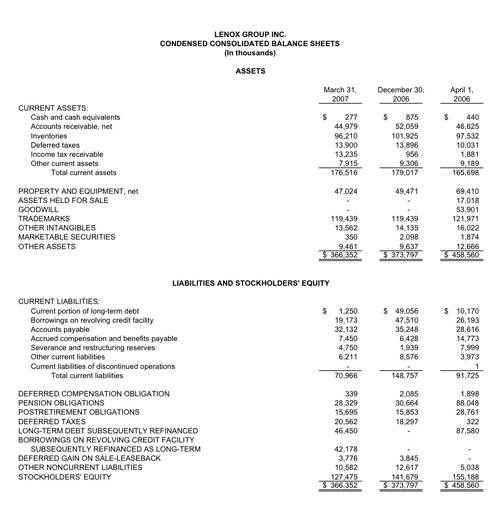

As previously reported, on April 20, 2007, the Company completed the refinancing of its revolving creditand term loan facilities by entering into amended and restated facilities totaling $275 million. These facilities consist of a $100 million term facility bearing interest at LIBOR plus 4.5% and a revolving credit facility of up to $175 million bearing interest at LIBOR plus an applicable margin ranging from 1.75% to 2.25%.

“These facilities provide us with the flexibility to finance the Company’s ongoing operations. The completed refinancing is an important step in positioning the Company to move forward with a stable financial platform for sustained profitability with the longer term financial flexibility needed to grow the business,” said Pfefferle.

First Quarter Performance

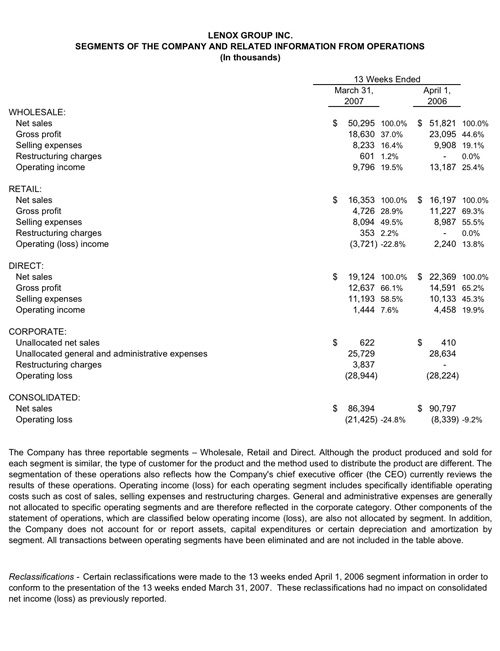

Wholesale Segment

Net sales decreased $1.5 million, or 3%, to $50.3 million in the first quarter of 2007 from $51.8 million in the first quarter of 2006, principally due to a continued reduction in net shipments of Department 56 branded product into its Gift & Specialty channel.

Gross profit as a percentage of net sales was 37% and 45% in the first quarters of 2007 and 2006, respectively. The decrease was principally due to higher levels of product liquidation through the wholesale channel during the first quarter of 2007 compared to the first quarter of 2006, and higher unfavorable manufacturing variances related to lower production levels at the Company’s silver manufacturing facility, which had an impact of four and two percentage points, respectively.

Selling expenses were $8.2 million, or 16% of net sales, in the first quarter of 2007 compared to $9.9 million, or 19% of net sales, in the first quarter of 2006. This decrease was principally due to lower sales as well as lower provisions for bad debt expense as a result of better than expected collections of overdue account receivable balances.

Restructuring charges were $0.6 million in the first quarter of 2007. The restructuring costs were principally severance costs related to organizational changes implemented as part of the Company’s new business plan.

Retail Segment

Net sales increased $0.2 million to $16.4 million in the first quarter of 2007 from $16.2 million in the first quarter of 2006. The increase in net sales resulted from higher same-store sales and a $0.7 million increase in net sales related to five new stores, which were open in the first quarter of 2007 but not open in the first quarter of 2006. Three of the five new stores were All the Hoopla stores that the Company has previously announced it will not continue. These increases were largely offset by a $3.1 million decrease in net sales from the closing of 28 Lenox retail stores throughout the first quarter of 2006. Same store sales increased by 16%, largely the result of focused promotional activity to liquidate excess inventory.

Gross profit as a percentage of net sales was 29% in the first quarter of 2007 versus 69% in the prior year period. During the first quarter of 2006, the Company held store closing sales for 28 stores operated under the Lenox trade name. The impact of this activity normally would have resulted in lower gross margins for the Lenox retail business; however, it was offset by a purchase accounting adjustment to value Lenox inventory at its estimated selling price less cost of disposal under the purchase method of accounting on the opening balance sheet date. The impact of this purchase accounting adjustment during the first quarter of 2006 was approximately $4.2 million, which increased gross profit as a percentage of sales by 25 percentage points, from 44% to 69%. In addition, gross profit as a percentage of net sales was lower in 2007 due to promotions aimed at liquidating excess inventory and the Retail segment’s focus on 2nd quality and excess products. On a go forward basis, the Retail segment has changed its focus to again making 1st quality product an integral part of its sales mix which, if successfully executed, should increase gross margins back to historic levels.

Selling expenses were $8.1 million or 50% of sales in the first quarter of 2007 compared to $9.0 million or 55% of sales in the first quarter of 2006, reflecting the operation of fewer retail stores in the first quarter of 2007 than in the prior year quarter due to the store closings that occurred in the first quarter of 2006.

Restructuring charges were $0.4 million. The restructuring charges related to the closing of a retail store in the first quarter of 2007.

Direct Segment

Net sales decreased $3.2 million to $19.1 million in the first quarter of 2007 from $22.4 million in the first quarter of 2006. The decrease in revenue was due to fewer new product promotions in the first quarter of 2007 compared to the first quarter of 2006 due to the continuation of delays experienced in the latter half of 2006 in developing and sourcing new product, which the Company believes it has now significantly addressed. In addition, the Company experienced lower customer response rates on product that was promoted in the first quarter.

Gross profit as a percentage of net sales was 66% and 65% in the first quarter of 2007 and 2006, respectively. The gross profit percentage of 65% in the first quarter of 2006 was negatively impacted by a purchase accounting fair market value adjustment related to the write up of inventory to its estimated selling price less cost of disposal under the purchase method of accounting on the opening balance sheet date. The impact of this purchase accounting adjustment was $1.2 million, which decreased gross profit as a percentage of sales by six percentage points for the first quarter of 2006. Excluding the impact of the purchase accounting adjustment, gross profit as a percentage of sales was 71% in the first quarter of 2006. The decrease in gross profit as a percentage of sales in the first quarter of 2007, when compared to the 71% in 2006, was primarily due to higher provisions for excess inventory.

Selling expenses were $11.2 million, or 59% of sales, in the first quarter of 2007 compared to $10.1 million, or 45% of sales, in the first quarter of 2006. The increase in selling expenses was primarily due to an increase in advertising targeted towards acquiring new customers which requires higher advertising expense as a percentage of sales.

Corporate

General and administrative expenses were $25.7 million in the first quarter of 2007 compared to $28.6 million in the first quarter of 2006, a decrease of $2.9 million. This decrease was principally due to a $2.0 million decrease in postretirement expenses related to the decision in the fourth quarter of 2006 to freeze the Company’s defined benefit pension plans and to discontinue offering postretirement healthcare benefits to current employees, a $1.3 million reduction in incentive equity compensation expense, and $1.8 million of various other cost reductions. Partially offsetting these cost reductions was $1.5 million of executive management consulting fees and $0.7 million of incremental product development expense related to the inclusion of Willitts in the first quarter of 2007 which was acquired during the second quarter of 2006.

Restructuring charges were $3.8 million in the first quarter of 2007. The restructuring charges related to $2.2 million of severance expense related to the Company’s previous chief executive officer, $0.8 million of lease buyout expense related to the shut down of the Company’s Rogers distribution facility, and $0.8 million of severance and other costs related to organizational changes implemented as part of the Company’s new business plan.

Provision for Income Taxes

The effective income tax rate was a 46% benefit in the first quarter of 2007 compared to a 38% benefit in the first quarter of 2006. The increase in income tax benefit was principally due to the recognition of $1.8 million of previously unrecognized tax benefits due to the expiration of the statute of limitations on certain tax positions in the first quarter of 2007.

Conference Call Information

Lenox Group management will review the company’s 2007 first quarter results on a conference call tomorrow, May 9, beginning at 9:00 a.m. (EDT). Investors will have the opportunity to listen to a live Webcast of the conference call over the Internet at www.earnings.com. To participate, please go to the Web site at least 15 minutes prior to the start time to register and download and install any necessary software. A replay will be available at the same location after the call concludes for those who cannot listen to the live broadcast.

About Lenox Group Inc

Lenox Group Inc is a market leader in quality tabletop, collectible and giftware products sold under the Lenox, Department 56, Gorham and Dansk brand names. The Company sells its products through wholesale customers who operate gift, specialty and department store locations in the United States and Canada, Company-operated retail stores, and direct-to-the consumer through catalogs, direct mail, and the Internet.

Forward-looking statements

Any conclusions or expectations expressed in, or drawn from, the statements in this filing concerning matters that are not historical corporate financial results are "forward-looking statements", within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. These statements are based on management’s estimates, assumptions and projections as of today and are not guarantees of future performance. Such risks and uncertainties that could affect performance include, but are not limited to, the ability of the Company to: (1) integrate certain Lenox and Department 56 operations; (2) achieve revenue or cost synergies; (3) generate cash flow to pay off outstanding debt and remain in compliance with the terms of its new credit facilities; (4) successfully complete its operational improvements, including improving inventory management and making the supply chain more efficient; (5) retain key employees; (6) maintain and develop cost effective relationships with foreign manufacturing sources; (7) maintain the confidence of and service effectively key wholesale customers; (8) manage currency exchange risk and interest rate changes on the Company’s variable debt; (9) identify, hire and retain quality designers, sculptors and artistic talent to design and develop products which appeal to changing consumer preferences; and (10) manage litigation risk in a cost effective manner. Actual results may vary materially from forwardlooking statements and the assumptions on which they are based. The Company undertakes no obligation to update or publish in the future any forward-looking statements. Also, please read the bases, assumptions and factors set out in Item 1A in the Company’s Form 10-K for 2006 dated March 15, 2007 and filed under the Securities Exchange Act of 1934, all of which is incorporated herein by reference and applicable to the forward-looking statements set forth herein.

Contact

Timothy J. Schugel

(952) 944-5600